|

||

|

|

||

|

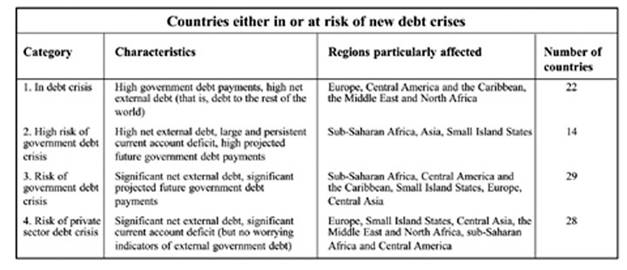

Debt is back! Rising inequality, along with financial deregulation, has spurred the significant increase in global debt levels. Although much of the media spotlight has focused on Greece recently, the fact is that more than 90 countries are either in or at risk of a new debt crisis. We reproduce below the executive summary of a new report by the Jubilee Debt Campaign which highlights this phenomenon. DEBT crises have become dramatically more frequent across the world since the deregulation of lending and global financial flows in the 1970s. An underlying cause of the most recent global financial crisis, which began in 2008, was the rise in inequality and the concentration of wealth. This made more people and countries more dependent on debt, and increased the amount of money going into speculation on risky financial assets. Increasing inequality reduces economic growth as higher-income groups spend a smaller proportion of their income on goods and services than middle- and low-earners. To tackle this problem, countries relied on either increasing debts or, for the countries which are the source of the loans, promoting exports through lending. This allowed growth to continue even though little income was going to poorer groups in society. Meanwhile, the rich were putting more of their growing share of national income into speculative lending and risky financial investments, in search of higher returns. Rising inequality, along with financial deregulation, therefore fuelled an unsustainable boom in lending and was an underlying factor behind the crisis which began in 2008. Global debt levels on the rise again International debt has been increasing since 2011, after falling from 2008-11. The total net debts owed by debtor countries, by both their public and private sectors, which are not covered by corresponding assets owned by those countries, have risen from $11.3 trillion in 2011 to $13.8 trillion in 2014. We at the Jubilee Debt Campaign predict that in 2015 they will increase further to $14.7 trillion. Overall, net debts owed by debtor countries will therefore have increased by 30% - $3.4 trillion - in four years. This increase in debts between countries is being driven by the largest economies. Of the world's 10 largest economies, eight have sought to recover from the 2008 financial crisis by either borrowing or lending more, thereby further entrenching the imbalances in the global economy. The US, the UK, France, India and Italy have all borrowed even more from the rest of the world. Germany, Japan and Russia have all increased their lending to other countries. The boom in lending to the most impoverished countries Alongside this increase in global debt levels, there is also a boom in lending to impoverished countries, particularly the most impoverished - those called 'low-income' by the World Bank. Foreign loans to low-income-country governments trebled between 2008 and 2013, driven by more 'aid' being provided as loans - including through international financial institutions, new lenders such as China, and private speculators searching overseas for higher returns because of low interest rates in Western countries. By looking at countries' total net debt (public and private sectors), future projected government debt payments and the ongoing income deficit (or surplus) countries have with the rest of the world, a Jubilee Debt Campaign report, 'The new debt trap', has identified countries either in or at risk of new debt crises. We have placed these countries into four groups (see table next page). Furthermore, while the 43 countries in groups 2 and 3 have worrying levels of externally held government debt, their private sector may be an even larger source of risk, given their high net debt levels and large current account deficits. Of the 14 countries we have identified as most dependent on foreign lending - those in group 2 - there are nine for which more data on projected future government debt payments is available from the International Monetary Fund (IMF) and World Bank: Bhutan, Ethiopia, Ghana, Lao PDR, Mongolia, Mozambique, Senegal, Tanzania and Uganda. The IMF and World Bank only carry out full debt sustainability assessments, which predict future debt payments, for low-income countries, countries which have recently moved from being low-income to middle-income, and a few small island states. As major creditors, the IMF and World Bank have a clear conflict of interest when conducting such assessments, but currently they are the only assessments available, and similar information for richer countries is not available at all. The nine countries for which data is available tend to have higher economic growth rates than other countries with similar incomes. Yet this faster growth does not correspond to similarly rapid progress in alleviating poverty, which is falling more slowly than the average for low-income countries. In fact, in five of the nine, the number of people living in poverty has increased in recent years, despite the fact that their economies have been growing rapidly in per-person terms. For example, in Ethiopia between 2005 and 2011, GDP grew by 60% per person, but the number of people living on less than $2 a day increased by 5.4 million. Furthermore, in all but one of the nine countries, inequality is rising. In Uganda in 2006 average income across the poorest 40% of society was $439 a year, but for the richest 10% $3,769. By 2013, the average annual income for those in the richest 10% had increased to $4,891, but for the poorest 40% to just $516. Finally, there is no evidence that any of the nine countries are becoming less dependent on primary commodities for their export earnings. Reliance on primary commodities, rather than manufacturing or services, makes countries more vulnerable to swings in volatile global commodity prices, and the earnings from commodities can more easily be captured by a small group of people. This means countries remain at heightened risk of debt crisis because falling commodity prices are a major source of economic shocks, and also because growth based on commodity exports often primarily benefits local and multinational elites, further increasing inequality. So although the countries that are most dependent on foreign lending have been growing quickly, poverty and inequality have generally been increasing, and there have not been significant structural changes to their economies that would make them more resilient to external shocks. High levels of lending mean that such shocks would be very likely to ignite new debt crises. Based on past experience, these would increase poverty even further and reduce funding for essential public services like healthcare and education. Public-private partnerships Lending and borrowing by the private sector is a major source of risk in terms of future debt crises. Another factor is the rise of 'public-private partnerships' (PPPs). This can mean many kinds of things. One is where the private sector builds infrastructure for a government, such as a road or hospital, and the government guarantees it will make set payments over a defined period. This has the same practical effect as if the government had borrowed the money and built the infrastructure itself, but it keeps the debt off the government balance sheet, making it look like the government owes less money than it actually does. In fact, the cost to a government is usually higher than if it had borrowed the money itself, because private sector borrowing costs more, private contractors demand a significant profit, and negotiations are normally weighted in the private sector's favour. Research suggests that PPPs are the most expensive way for governments to invest in infrastructure, ultimately costing more than twice as much as if the infrastructure had been financed with bank loans or bond issuance. The UK led the way in developing and implementing such schemes, known there as the Private Finance Initiative (PFI), in the 1990s. A 2015 review by the UK's National Audit Office found that investment through PFI schemes cost more than double in interest payments than if the government had borrowed directly, even without taking into account the cost of paying private companies profit under PFI. This disastrous record has not stopped the UK government promoting PPPs across the world. For example, it set up and funds the Private Infrastructure Development Group (PIDG), itself a PPP, which exists to promote PPPs in the developing world. Such PPPs may be hiding a huge amount of payment obligations, reducing the money available to future governments and increasing the threat of future debt crises. PPPs are currently thought to account for 15-20% of infrastructure investment in developing countries. Falling commodity prices The debt crisis which began in much of the global South in the early 1980s was triggered by falling prices for primary commodity exports, and an increase in US interest rates. This means countries were earning less money but spending more on their debts which were primarily owed in dollars. Since early 2014, many commodity prices have fallen significantly. For affected countries, the loss of expected export income has caused currency devaluations, because it has reduced the amount a country is earning from the rest of the world and therefore increased the relative cost of debt payments made in foreign currencies. In Ghana, official figures are not yet available but we calculate that because of currency devaluation, government foreign debt payments in 2015 will have increased to 23% of government revenue, from an IMF- and World Bank-predicted 16%. In Mozambique, payments are estimated to have risen from 8% of revenue to 10%. Neither estimate takes into account any drop in government revenue from lower commodity prices. Furthermore, while commodity prices have fallen, interest rates on the major currencies in which loans are issued have not risen - yet. US dollar interest rates are expected to increase later in 2015. Such rate increases could dramatically affect the relative value of government debts in dollars, and countries' ability to repay them. Major interventions are needed Making the global economy less prone to booms and busts, and countries more resilient and less prone to debt crises, requires major structural changes to reduce the speculative activity which fuels them. One of the causes of global financial instability has been increasing inequality. Inequality should clearly be tackled in the interests of fairness and justice and because it is vital in promoting well-being, but doing so would also directly help create a more stable financial world, by making lower-income groups less dependent on debt and reducing the amount of money that high-income groups put into speculation. Reducing inequality depends on a range of actions, such as strengthening trade unions and workers' rights so that a greater share of income accrues to workers rather than speculators, and taxes on wealth as well as income to enable greater redistribution. For currently impoverished countries to become more resilient to global economic changes, they need to be less dependent on primary commodity exports. Gaining other sources of income will require a whole range of government interventions depending on the situation of the country concerned. The freedom of governments to determine and implement the measures needed should not be undermined by international trade treaties or policy conditions attached to international loans and development aid. Preventing debt crises requires action by both borrowers and lenders. As we are based in London, one of the world's major financial centres, Jubilee Debt Campaign's primary responsibility is to argue for systemic change to lending to help end the cycle of debt crises. In the last section of our 'The new debt trap' report, we outline a range of policies that lending governments, including the UK, could support now to make lending more responsible and help prevent future debt crises. These include: 1) Regulating banks and international financial flows. 2) Creating a comprehensive, independent, fair and transparent arbitration mechanism for government debt. 3) Supporting cancellation of debts for countries already in crisis. 4) Supporting tax justice. 5) Ceasing to promote PPPs as the way to invest in infrastructure and services. 6) Supporting responsible lending and borrowing. 7) Ensuring aid takes the form of grants rather than loans, and that 'aid' loans do not cause or contribute to debt crises. The above is the text of the executive summary of 'The new debt trap: How the response to the last global financial crisis has laid the ground for the next', a report by the Jubilee Debt Campaign (July 2015). The full text of the report, written by Tim Jones, is available on the Campaign's website www.jubileedebt.org.uk.

*Third World Resurgence No. 298/299, June/July 2015, pp 5-7 |

||

|

|

||